Your Credit Score.

And More.

Anytime. Anywhere.

Staying on Top of Your Credit Has Never Been Easier.

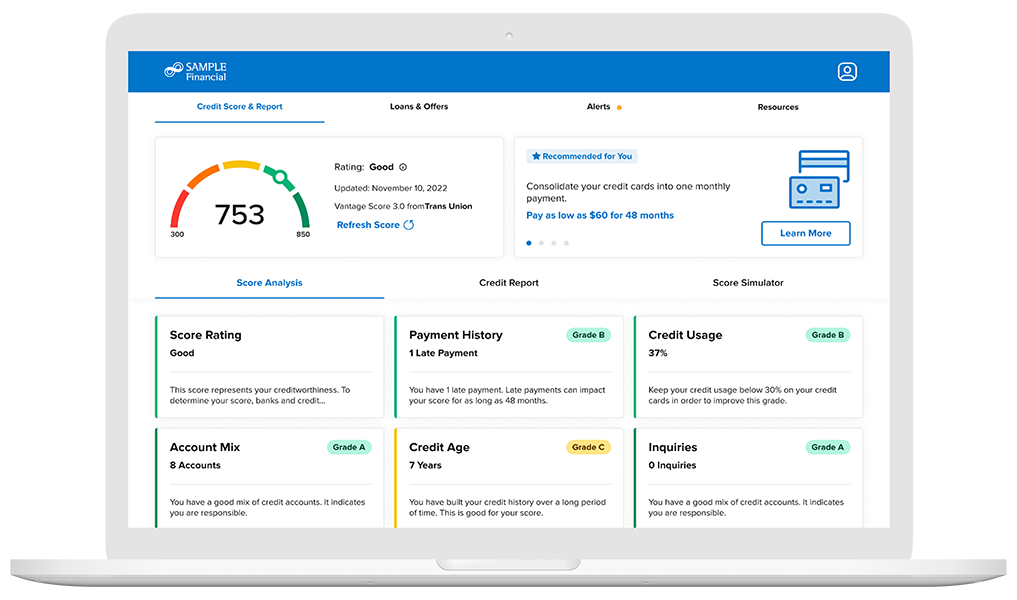

With one powerful tool, access your credit score, full credit report, credit monitoring, financial tips, and education.

All of this without impacting your credit score!

You can do this ANYTIME and ANYWHERE, for FREE, thanks to your Credit Union.

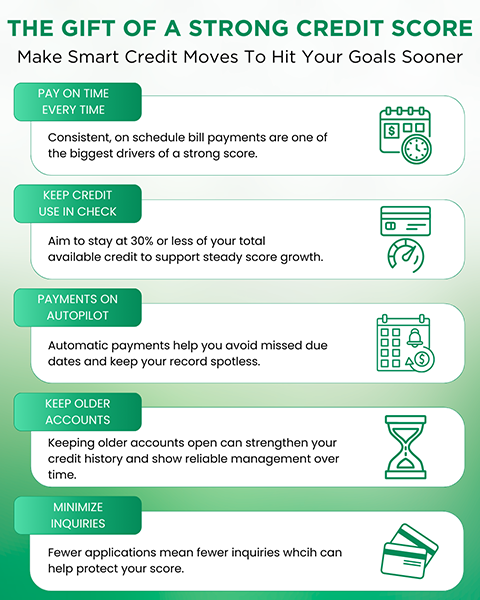

The Benefits of Credit Score & More:

How to Enroll in Credit Score Today:

Option 1: Online Banking

- Log in to online banking.

- Navigate to the Credit Score & Report widget (at the top right column)

- Click on the “Show Full Report” button on the widget to enter.

- If you have not yet, you will need to accept the terms of service to gain access to the service.

Option 2: Mobile App Banking

- Log in to the mobile app on your smartphone or tablet.

- Tap on the “Credit Score & Report” widget (listed at the top of the list of widgets on the Home page).

- You will be taken to the SavvyMoney/Credit Score & Report launch page.

- Tap “Go to SavvyMoney” to enter the widget.

- If you have not yet, you will need to accept the terms of service to gain access to the service.